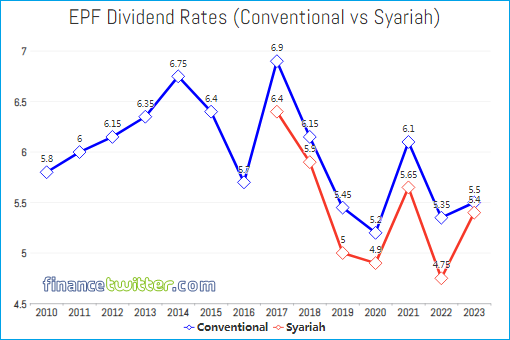

According to finance twitter , for financial year 2023, the EPF (Employees’ Provident Fund) or KWSP has announced higher dividend for both Conventional savings (5.5%) and Syariah savings (5.4%). In previous year (2022), EPF had declared 5.35% and 4.75% dividend rates for Conventional and Syariah respectively. However, despite higher dividends for last year, suspicion arose over its distributions.

While total investment income stunningly increased by 29% year-on year for the financial year ended Dec 31, 2023 – skyrocketing from RM51.91 billion in 2022 to RM66.99 billion – the Conventional dividend only increased by 0.15% compared to Syariah’s 0.65% jump. Either fund managers of Conventional investment sucks or the investment team in charge of Syariah’s investments were genius.

There is, however, another possibility – the EPF could have silently diverted profits and dividend from Conventional to Syariah for political reason. The EPF has always paid lower dividends for syariah account members largely because the savings are forbidden from investments linked to “riba” (interest), “maysir” (gambling) and “gharar” (uncertainty in contracts).

Essentially, when the EPF decides to invest Syariah savings in Syariah assets, it has no exposure whatsoever to the global conventional banking system, mainly global banks and global insurance companies, which are able to achieve higher investment returns. What they are allowed to invest are sectors such as oil and gas, automobiles and parts, as well as mobile telecommunications.

Introduced in January 2017 as an option for members who wish to have their retirement savings managed and invested in accordance with Syariah principles, the gap between Conventional and Syariah dividends had never been this small. In 2017, the difference was 0.5%, 2018 (0.25%), 2019 (0.45%), 2020 (0.30%), 2021 (0.45%) and 2022 (0.60%).

Interestingly, in March 2023, the Employees’ Provident Fund announced that it planned to manage its conventional and syariah portfolios separately in order to get better returns from the Islamic investments effective January 2024. Its CEO Amir Hamzah Azizan said – “We want to give a better chance for syariah investments to get higher returns”.

Therefore, it’s highly suspicious that the latest 2023 dividends had been manipulated to create an impression that under Prime Minister Anwar Ibrahim, who has been trying desperately to win over Malay Muslim vote bank, the Syariah savings suddenly could generate extraordinary dividends at the expense of Conventional savings.

There’s nothing wrong for EPF to get better returns from Islamic investments. After all, it was established to provide an avenue for Muslim members to have Syariah-compliant retirement savings such as for performing Hajj (pilgrimage) and Umrah, as well as for their family. It is also to enable members (upon death) to provide halal fund to be distributed to the heirs as inheritance.

But due to lack of transparency, EPF members could only suspect that their Conventional savings’ dividend had been robbed or siphoned to reward the Syariah savings. As far as the retirement fund is concerned, it would be as easy as shifting profits from left to right. In the same breath, Muslim members do not know if their Syariah savings are being rewarded with non-halal returns.

For obvious reasons, the EPF does not share the details of portfolios between the two types of savings. Worse, its investment portfolio of over RM1 trillion is being managed based on a single strategic asset allocation – 47% in fixed income, 42% in stocks, 7% in real estate and infrastructure and 4% in money market instruments. So, how do members know which is which?

The total payout – RM50.33 billion for conventional and RM7.48 billion for syariah – means after minus RM57.81 billion in dividends, EPF keeps the remaining RM9.18 billion of income. And we have not even talked about its investment assets, which hit a strong growth of RM1,135.82 billion, an increase of 13% compared to RM1,002.67 billion in 2022.

The best part is the local stock market – FBM KLCI – saw negative growth with the KLCI declining 2.7%. The EPF’s participation in the Bursa Malaysia in terms of value traded was 23% for FBM100 stocks and 31% for FBMKLCI stocks. This is the primary playground of Syariah savings because, theoretically, it can’t venture into Western non-halal investments.

To lend credence that conventional had performed way better than syariah, a total of RM58.97 billion out of the RM66.99 billion total investment income was generated for Conventional savings, and only RM8.02 billion for Syariah savings. This means conventional contributed a whopping 88% income of EPF, whilst syariah only generated 12% – a ratio of almost 9:1.

It’s worth to note that as of 30 September 2023, the EPF’s investment assets amounted to RM1,092.32 billion, comprising 39% Syariah assets and 61% conventional assets. Again, the syariah to conventional ratio of 4:6 shows that every RM6 conventional assets had generated RM9 in profit, compared to syariah’s RM4 that could generate only RM1 in return.

In order to comply to ethical investment practices that avoid sectors such as alcohol, gambling, adult entertainment, and military weapons, Syariah savings had to employ a rigorous syariah screening process and appropriate syariah contracts in its investment. As a result, it’s options are rather limited. So, how could the dividends gap between syariah and conventional be only 0.1%?

About 62% of the investment assets were invested domestically, generating RM31.71 billion (47% of total investment income) while global assets generated RM35.28 billion (53% of the total investment income). This means global investments could generate twice as much income as domestic investments. Of course, EPF is forced to support local business or stock market, without which the KLCI would collapse.

2023 was supposed to be a tough year for stocks and the economy. But that wasn’t the case with foreign equities, especially in the United States. The S&P 500 was up about 24% last year. Driving the S&P 500’s returns in 2023 was the force of the “Magnificent Seven” – Apple, Amazon, Nvidia, Tesla, Microsoft, Meta, and Alphabet. Hence, EPF’s conventional portfolio would be richer by 24% just by investing in S&P500.

That perhaps explains why conventional savings generated 88% income for EPF. No matter how you look at it, it does not deserve the low dividend. It should get at least 6.5% instead of 5.5% due to the bullish global returns. Even in 2021, it could declare 6.1% dividend at a time when the country was struggling with Covid-19 recovery. To declare 5.5% means the country’s economy is worse.

During Najib Razak era (2009-2018), the retirement fund had never declared dividend less than 5.65%, with 6 years above 6% – ranging from 6.0% (2011) to 6.9% (2017). Is Malaysia now worse under Prime Minister Anwar Ibrahim, despite claims of bullish economy, low inflation, high employment, flushing investments and whatnot?

At best, the Employees’ Provident Fund had diverted Conventional savings’ rightful dividend to Syariah savings to strengthen PM Anwar’s Islamic credential. At worst, the dividend may have been siphoned – quietly – to the finance ministry to cover-up expenses such as special appreciation aid, special allowance, early incentive payment and whatnot for civil servants to boost Anwar’s image as the Malay champion.

Source : Finance Twitter

The Coverage Malaysia